The shift to prioritizing the adjuster experience

When the 20-year veteran adjuster opens a new water damage claim, they know in 30 seconds whether it's a two-week or a two-month file. They've already flagged the subrogation potential, validated the right coverages, and drafted the first policyholder email, the one that prevents the angry call to customer service three weeks from now. They already know which vendor they're assigning. The task is in the queue before they can take another sip of coffee.

Two desks over, the junior adjuster (all the drive in the world, but only 18 months in) opens an identical claim. They don't have instant recall of the hundreds of similar files they've already worked on, so they don't know the right contractor on reflex or have a vetted shortlist of twelve specialists they're certain will deliver. They ask an already-antsy policyholder a few too many questions up front, drop the ball on one contractor email, and suddenly it's been three weeks. So that frustrated policyholder call lands in your support queue after all.

Execution variance: wildly different outcomes for the same type of claim. It's not a problem you hire your way out of, and it's the most expensive line item in claims that never shows up on a report.

But, carriers have always had a workaround: route the high-value, high-touch claims to your most senior adjusters, and let the up-and-comers cut their teeth on higher-volume, more common files to "get up to speed." And, technically(?), it's worked.

But what happens when the expertise keeping that wheel turning walks out the door? Adjusters leave. They retire, change careers, change geographies. There are a number of reasons the institutional knowledge that entire processes were built on can simply walk off. And when it does, every conventional fix that depended on decades of pattern recognition, vendor relationships, and entrenched know-how is suddenly useless.

The “pitch of the moment” misses the point

Basic automation is relatively simple to do. It’s also a generously uncomplicated path to impact when you’re talking about fundamental automations replacing legacy processes that were years behind on an overhaul.

And that type of quantifiable impact makes it easier for teams to advocate for more of it, and, generally speaking, carriers are happy to oblige. When every vendor pitch can promise them those same immediate results, where could there be a downside?

Glad you asked.

Watch a high-performing adjuster work, and the patterns are obvious in seconds. Same checks on every file, same steps to validate coverage, the first email to the policyholder already teed up. They're so practiced that it barely requires a conscious commitment anymore. They've simply watched it work, file after file, for years.

So the obvious move, when AI and automation take the stage, is to package those steps into knowledge bases and automated workflows and make them the new standard for every adjuster on staff. Encode the best, distribute it to everyone. Oh so simple.

Except that pitch — that every point solution flooding the market has its own version of— misses the thing that made those workarounds possible in the first place.

Accounting for what can’t be encoded

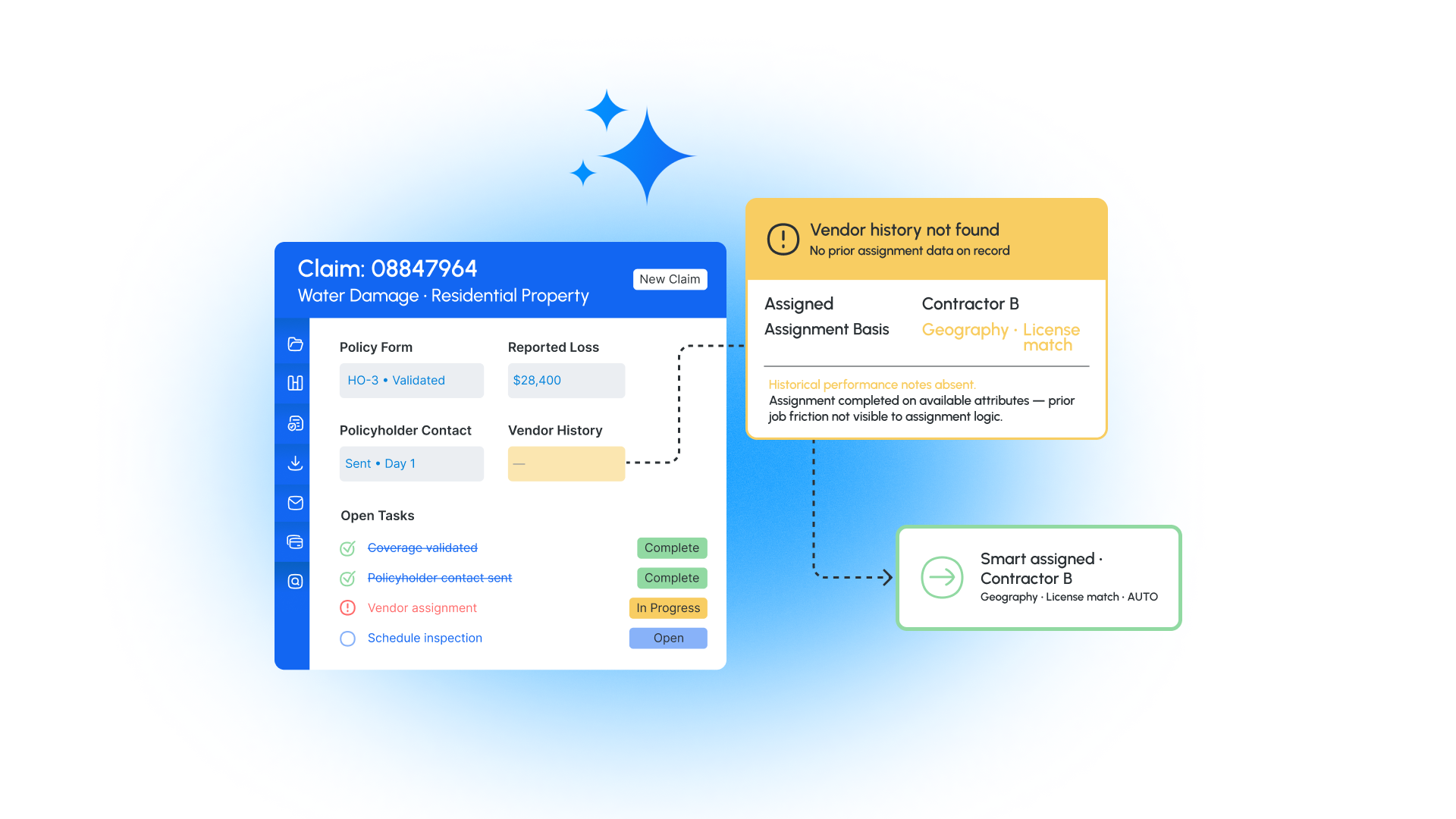

On paper, Contractor A and Contractor B are interchangeable: both licensed, validated water-damage specialists, fully capable of performing the work for a water damage claim. The only difference the system can see is that B is ten miles closer to the policyholder; two good options, and one decision to make.

An agentic triage agent makes it instantly, and it picks B. On all counts, it’s the right call. Contractor B is validated, available, and closer, so there's nothing to flag. A no-brainer.

The veteran adjuster picks A. Not because he’s rogue on rules, but because of something the rules can't see: Contractor B has a habit of small slips on jobs with stucco homes. Nothing major, never a formal complaint, just the kind of friction the veteran has quietly smoothed over enough times to stop sending through those particular jobs. That instinct isn't written down anywhere, and it isn't in the data. The adjuster hardly even thinks about it. It’s the residue of a hundred prior files living in one person's head, and it's the whole reason A was the better call.

The automation did everything right, and it still costs you. Triage is flawless, contractor is on site in two days, and three weeks later, Contractor B slips on the work order exactly the way the veteran knew it might. The frustrated policyholder call still lands in your queue, and no one can point to the step where it went wrong, because there wasn't one. The process was followed to perfection, but it never contained the thing that mattered.

Recognizing what can’t be automated around

And now, for the trap. Once you see this, the instinct is to give the AI more room: let it use judgment, let it weigh the soft factors the way a veteran would, let it pull context from here, and here, and here. The evolving expectations for AI fit the same bill as every technology movement before it: more, more, more.

But here, it’s not the right call.

An AI with the latitude to make those calls on its own is an AI taking liberties, in a world where the wrong liberty can be a coverage decision, a compliance exposure, or a settlement you can't claw back. The very thing that would let it catch the Contractor B problem — the freedom to act on instinct without a concrete rule behind it — is exactly the thing you can't safely hand it.

So you can't encode your way to the nuance because the signals aren't in the data, and you can't autonomize your way to it either because the autonomy that would help is the autonomy you can't allow. The human-ness between the lines has been quietly shaping outcomes for years, and a shiny new point solution will never have the context to see it.

Now, let’s add that the customer experience can't be a casualty of efficiency. Not in a world where it's never been easier for a policyholder to change carriers, and roughly half of them say a single poor claims experience would be enough to make them do it.

Both problems put carriers in the same place

Whether the tool is too rigid to see nuance or too loose to be trusted, the result is the same: adjusters abandon it, it never makes an impact, and the shiny new solution dies in some forlorn dashboard not even three months later.

Nice to see you again, pilot purgatory.

Adjusters are busy, and another tool stacked on top of systems they may already find frustrating isn't exactly a motivator. They won't adopt something that (a) doesn't make their job easier, or (b) looks like it's trying to do their job but does it worse, creating messes they know they'll be the ones to clean up. Every adjuster is attached to different parts of their process, and that attachment is never the same from one person to the next.

What they do want is to bring new tools in intentionally, in ways that make sense to them, at a pace they’re comfortable with. They do want to tweak and tailor it to the way they work (they would just prefer to do it once).

AI for the sake of AI is where failures happen. AI for the sake of the adjuster experience is where wins happen.

So… how do you fix it?

The honest answer is: it depends.

But it’s not as simple as "automate what's routine and let adjusters handle the high-value work." No senior adjuster is going to mourn losing fifteen run-of-the-mill auto claims a week to touchless processing, but that approach silos your impact to one claim type, one loss type, one line of business. Which means the whole operation is set up to plateau almost immediately.

Every adjuster, claim type, vendor, and policyholder is different. ”It depends" isn't a dodge. It’s an accurate answer, and pretending there’s a definitive answer that works in every scenario is the reason point solutions keep stalling.

You don’t have to fix what doesn’t break

The fix for both dead ends is the same, and it's structural. Not an agent that takes liberties. Not a tool that executes blindly and misses the context. Infrastructure: AI that lives in the system of record and works from the ground up, so it doesn't get forced on adjusters at every click and doesn't run off making decisions it has no business making. It scaffolds judgment and makes a distinct space for it rather than rushing to replicate it or replace it.

In practice, that rests on four things:

Data readiness. Adjusters need instant, real-time access to everything available on a claim, the moment they need it (a note that the data needs to be clean, accurate, and up-to-date)

Single source of truth. One system where everything happens on a claim. Cross-channel communications, vendor management, financials and deductibles, tracking and issuing payments. One place… not seven tabs, two portals, three apps, a spreadsheet, and a whiteboard.

Proactive, intuitive action. Co-pilot capabilities, the adjuster controls (alerts, task creation and assignment, on-demand QA checks, and health scores) that fire where and when the adjuster wants them, not where a vendor hard-coded them.

Ease of use. Easy to deploy, easy to navigate, easy to iterate. If it isn't, none of the above matters, because no one will touch it.

Build it this way, and adoption stops being a battle. The institutional expertise seeps in from the foundation instead of being pushed down from the top, and because the adjuster never has to fight it, they actually use it.

Most AI ROI projections in insurance are ceiling stories: best case, best data, best execution. Carriers are better off starting with replacing the floor.